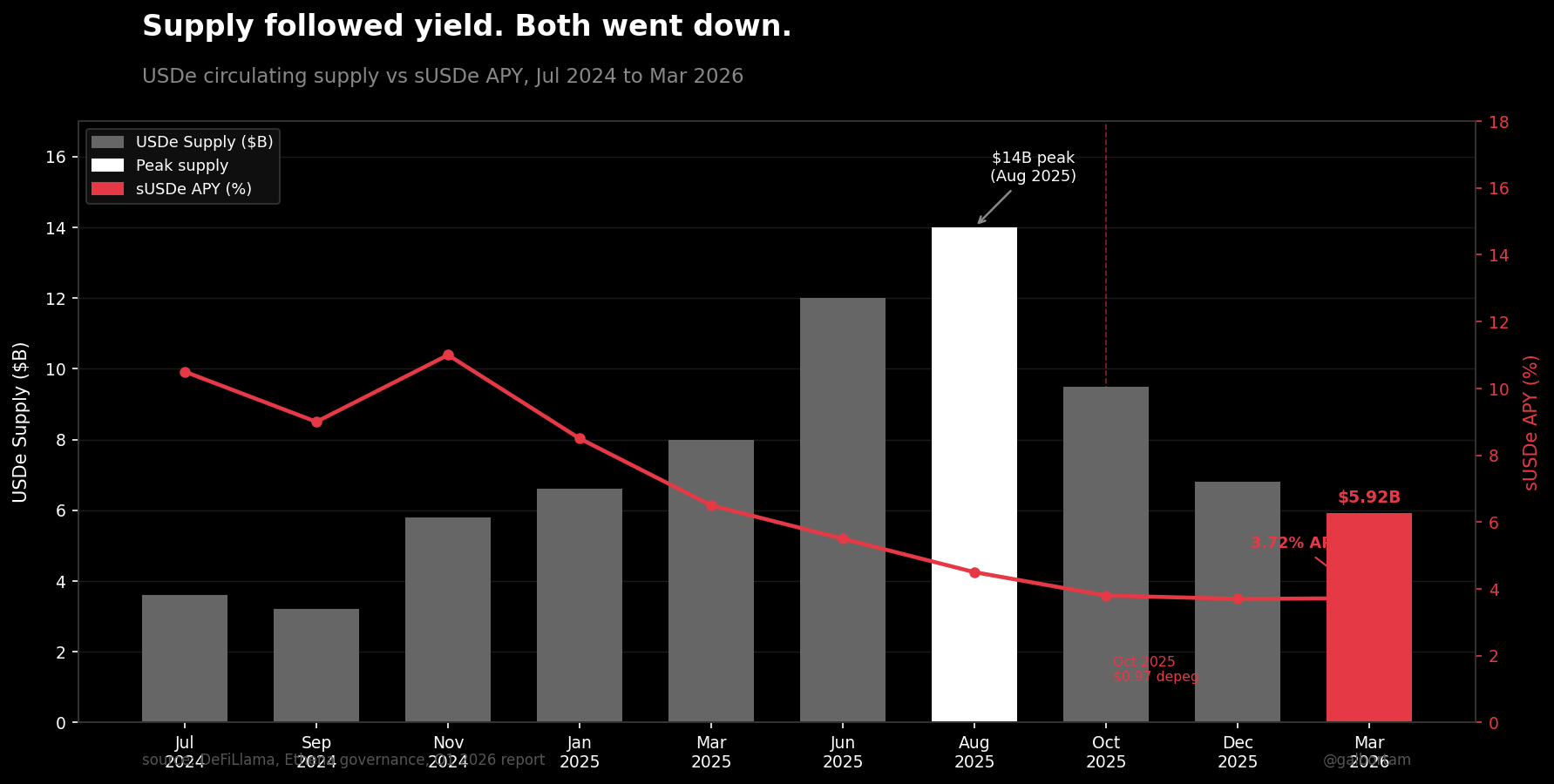

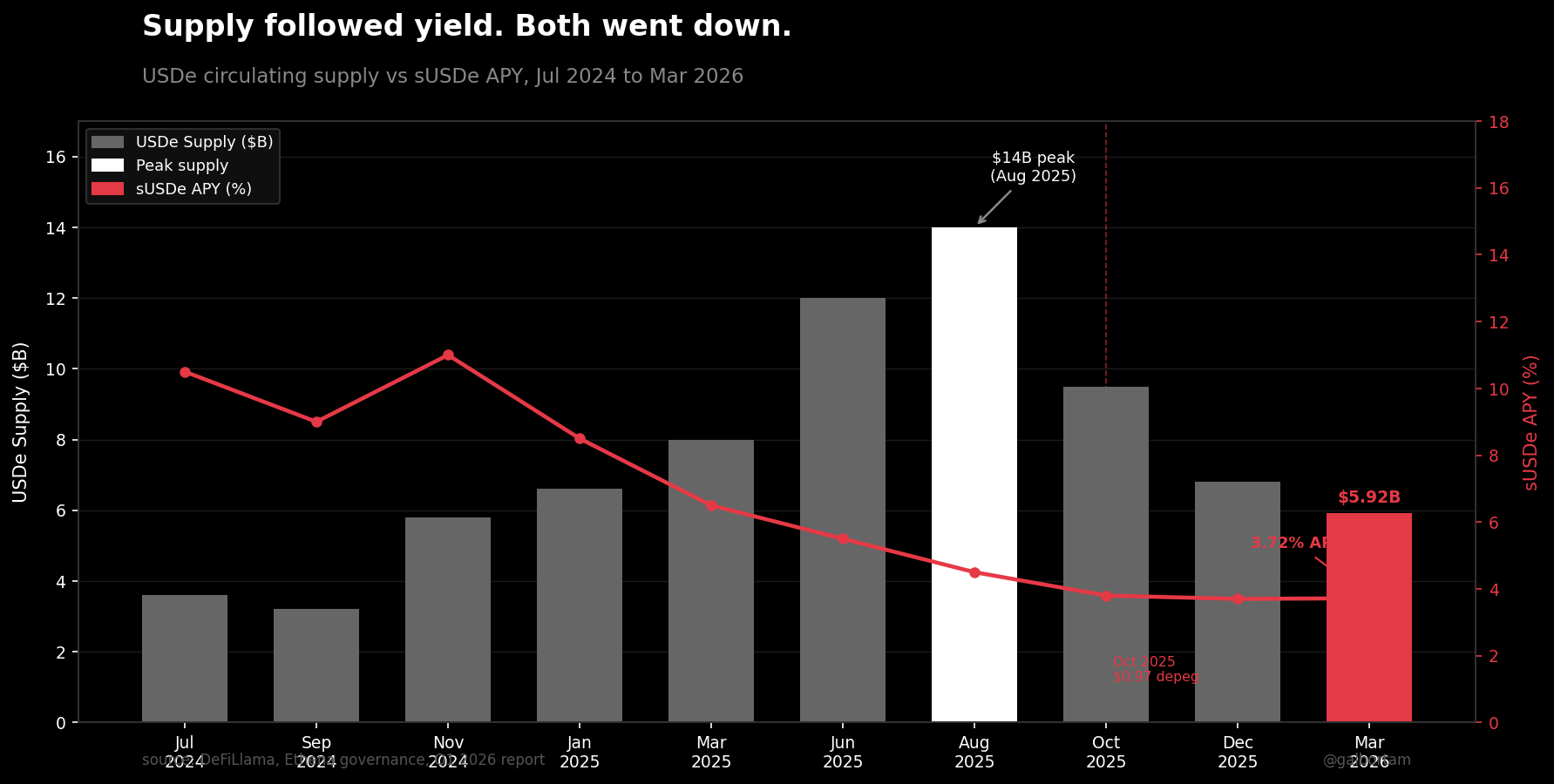

Ethena's supply didn't fall because of a hack or a governance failure. It fell because the carry trade stopped paying.

That's the actual stress test. $8B in capital exited in three months once the Aave-Pendle loop stopped making sense. The $0.97 depeg in October 2025 lasted hours. The supply collapse lasted a year.

How USDe Works

Ethena mints USDe by taking ETH (or BTC) as collateral and opening a short perpetual futures position against it. The collateral earns staking yield; the short earns funding rates when longs dominate the market. Together they produce the sUSDe APY.

The delta-neutral structure means USDe holds its dollar peg regardless of ETH price moves. The peg risk isn't a price crash. It's a funding rate crash.

The Numbers

In early 2025, Ethena held 93% of its backing in perpetual futures positions. Today that number is 11%. The other 89% is in stablecoins, Treasury products, and lending positions.

The protocol didn't redesign itself. The supply contracted, and what remained was the safer, lower-yield layer. At $14B supply with 93% perp exposure, the risk profile was completely different from today's $5.92B with 11% exposure.

sUSDe now yields 3.72%. The 2024 average was 11%. The 2025 average was 5%. Each compression wave drove out a layer of capital, and each capital exit further reduced perp exposure, which further reduced yield. The loop runs in both directions.

The reserve fund stands at $62M. LlamaRisk's conservative stress scenario requires $23M at current perp exposure levels. The $62M figure looks strong, but that's partly because the denominator shrank: at $14B supply and 93% perp backing, $62M covered far less tail risk than it does today.

The Procyclical Risk

Here is what the stress test actually revealed: Ethena's risk profile is procyclical. When funding rates rise, new capital enters, supply expands, and perp exposure grows with it. That's when the reserve-to-exposure ratio tightens and the carry-reversal risk accumulates.

The protocol is safest when conditions are worst. It is most exposed when conditions look best.

What This Means For You

If you're allocating to sUSDe: the 3.72% yield prices in smart contract risk, CEX custody risk, and carry reversal risk combined. That's roughly 50-100 basis points over T-bills. Whether that's adequate depends on how you weight each risk, but the margin is thin.

If you're building on USDe as collateral: the supply can move $8B in a quarter when the carry trade shifts. Any integration that assumes stable supply depth is stress-testing against the wrong scenario. The question isn't "does the peg hold" — it's "does the supply stay deep enough to matter?"

What to Watch

Track the perp backing percentage at app.ethena.fi/dashboards/hedging. When it rises back above 50%, the old risk profile is returning. That's when the reserve-to-exposure ratio warrants a second look.

The second signal: if sUSDe APY rises above 8%, carry chasers return, the Aave-Pendle loop activates, and supply expands fast. A rising APY is not a green light. It's a warning that concentration risk is building again.

GAM Analysis is independent DeFi protocol research by @galbortam. If someone forwarded this to you, subscribe here.