If you are holding SYRUP because Maple is growing, that growth does not flow to the token directly. Three layers of fee extraction sit between borrower interest and any value reaching SYRUP buyers. Each one takes its cut.

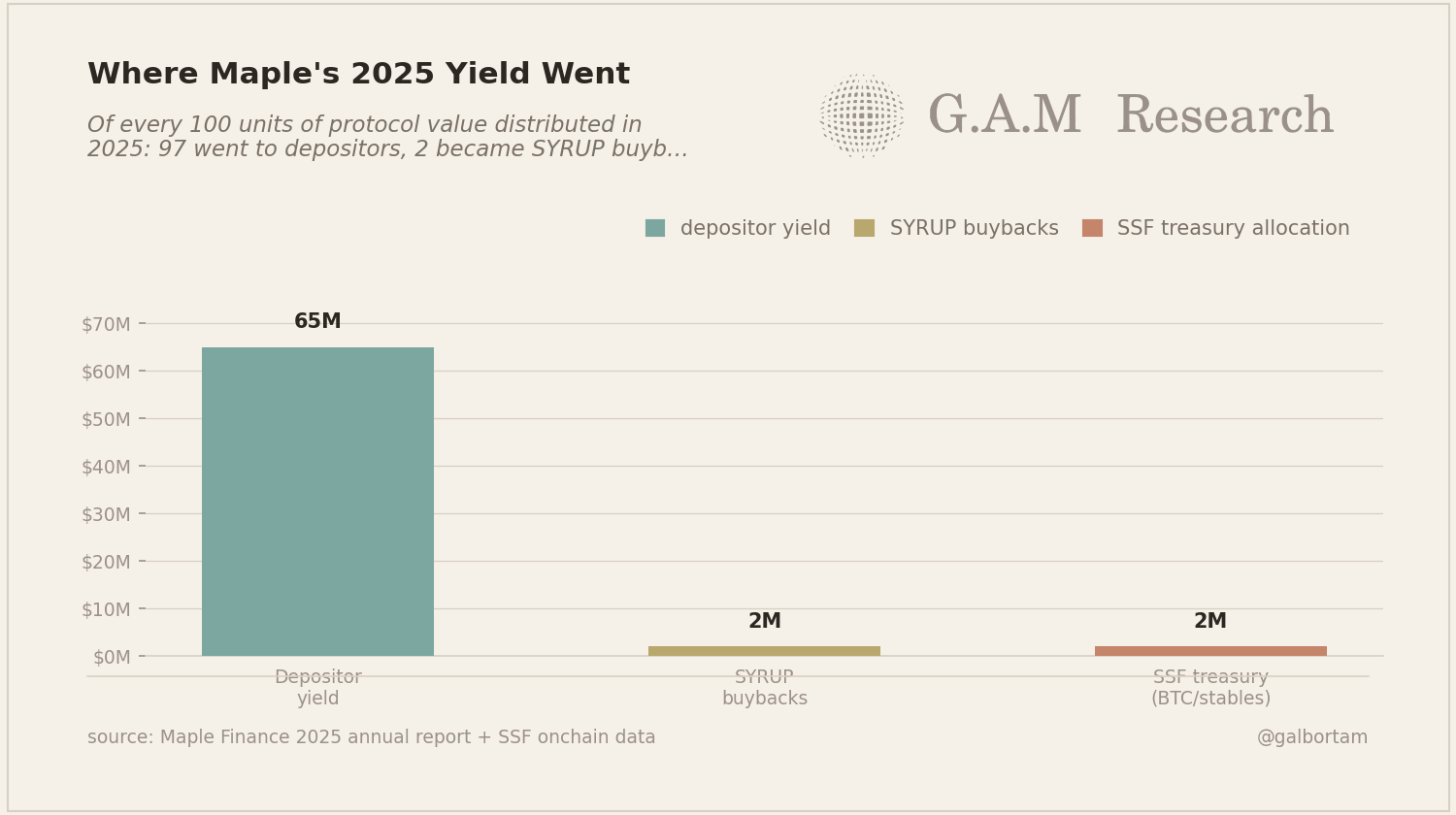

In 2025, Maple paid 65M USD in yield to depositors and executed just over 2M in SYRUP buybacks. AUM grew from 516M to 4.59B. The buyback mechanism that was supposed to tie token value to protocol revenue launched in November 2025, five months ago.

How the money moves

Maple runs three products: syrupUSDC, syrupUSDT, and Maple Institutional-Secured Lending. The first two are permissionless yield-bearing tokens available to any wallet. The third targets accredited allocators at 10.31% APY on secured loans.

Borrowers pay gross interest. Maple takes a management fee of 12% on monthly interest payments for direct loans. Depositors receive the net yield, roughly 7-8% base APY on syrupUSDC.

Pool delegates earn 33bps per loan origination on top of the management fee. The remainder of protocol fee revenue is Maple to deploy.

MIP-019 passed October 31, 2025, with over 99% of participating governance. It sunset staking rewards entirely and created the Syrup Strategic Fund. The SSF receives 25% of ongoing protocol revenue. It uses those funds for SYRUP buybacks, BTC accumulation, and stablecoin treasury building.

The numbers

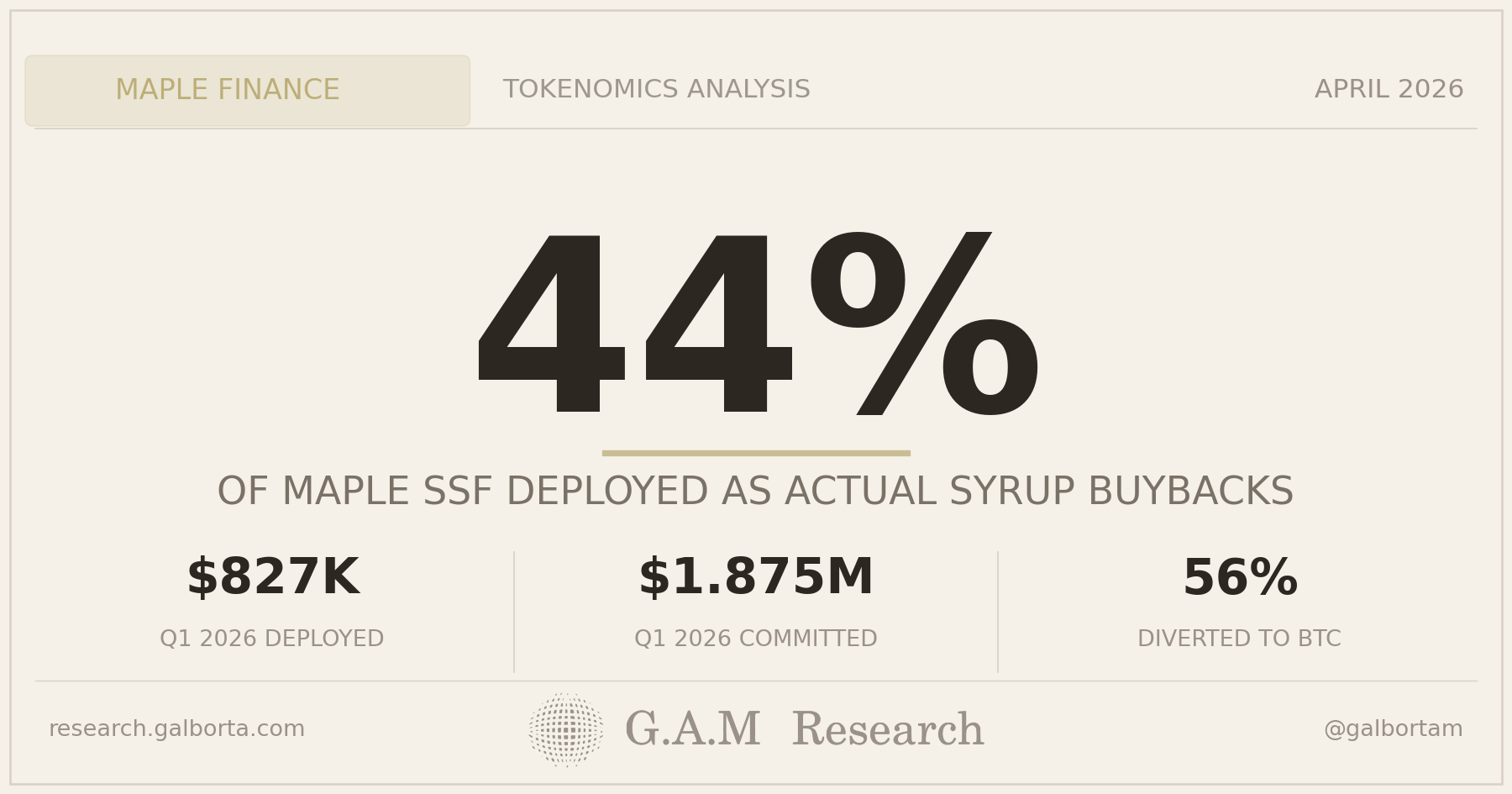

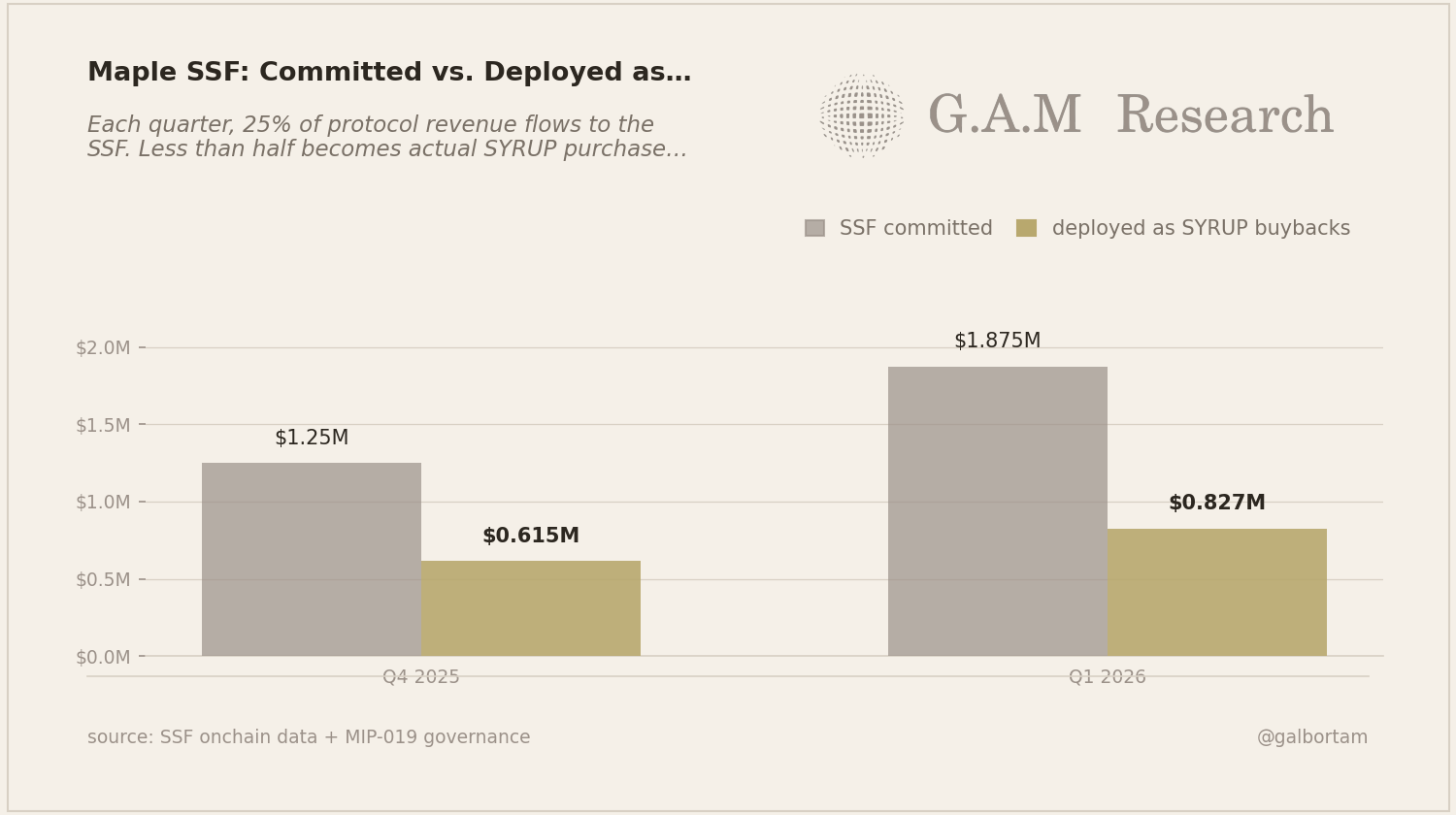

Depositors received 65M USD in yield. Protocol fees for the year ran roughly 15-17M. At 25% SSF allocation, the theoretical annual commitment was 4-5M. Actual buybacks executed: 2M.

The 65M to depositors versus 2M in buybacks is not a timing issue. It reflects where each stream comes from.

Depositors earn directly off gross borrower interest. SYRUP holders earn off the fee residual after depositors have been paid. Then only the fraction the SSF deploys as actual purchases reaches the token.

The 32:1 ratio between depositor yield and buybacks is the structure, not a rounding error.

The SSF deployment breakdown:

- Q4 2025: 615K deployed vs 1.25M committed. Ratio: 49%.

- Q1 2026: 827K deployed vs 1.875M committed. Ratio: 44%.

- Annualized pace: 3.3M in actual buybacks.

The governance proposal committed 25% of revenue to the SSF. It did not specify what fraction goes to buybacks versus BTC and stablecoins. One community member explicitly asked during the vote whether the full 25% will be used for token buybacks. The official response did not directly answer.

At 3.3M annualized and a 295M market cap, the implied buyback yield is 1.1%.

Why staking was removed

The prior model gave SYRUP stakers token emissions (inflationary, dilutive) and fee-based buybacks. MIP-019 removed emissions entirely. Stakers now receive only whatever the SSF deploys as buybacks.

The stated logic was that buybacks create more durable value than emissions. That holds when the buyback volume is large enough to compress supply materially. At 3.3M annualized against 1.16B circulating tokens at 0.25 each, the compression effect is less than 0.1% of supply per year.

The stress test published three weeks ago found that bad debt comes from depositor NAV, not the SYRUP treasury. The tokenomics data adds the other side of that design: when loans perform well, depositors receive the primary yield stream first. The governance token earns on what remains. Both relationships flow from the same structural choice: Maple sells yield products, and the governance token captures the protocol economics above and beyond depositor returns.

What this means for allocators

The SYRUP thesis requires two independent things to happen.

First: Maple reaches 100M ARR by end of 2026. The current Q1 run rate was 30M annualized. Reaching 100M means more than tripling from here. The 5B AUM and 60 institutional borrowers give the growth a real foundation, but the runway is significant.

Second: The SSF deploys into buybacks rather than treasury diversification. In Q1 2026, it deployed 44% as actual buybacks. If that ratio holds at 100M ARR, the real buyback yield is 3.7%, not 10%. If the team leans toward treasury building as AUM grows, the ratio compresses further.

Both variables are unknowns. The market cap of 295M is pricing some combination of optimistic assumptions on both.

What this means for builders

If you are integrating syrupUSDC as collateral or using the yield product, the depositor economics stand on their own: 7-8% base APY on secured institutional loans, 2.15B outstanding, 99% repayment rate in 2025. The product works as described.

The SYRUP token is a separate claim. Depositing into syrupUSDC and holding SYRUP expose you to different return profiles. The deposit earns off gross borrower interest. The governance token earns off the fee residual after depositors have been paid, minus the SSF treasury allocation, minus whatever fraction of the SSF goes to non-buyback assets.

What to watch

Monthly SSF deployment, available onchain. The SSF has been live for five months and has shown a flat pace: roughly 270K-280K per month.

The specific threshold: Monthly protocol revenue crossing 4M. At that run rate, 25% SSF = 1M per month committed. If deployed at 44%, that is 440K per month in buybacks, or 5.3M annualized, a 1.8% buyback yield against the current cap. When monthly buyback execution exceeds 500K, the SSF deployment ratio is improving. When it holds at 275K while ARR climbs, the gap is widening, not closing.

One more thing

Maple originated 11.27 billion in loans across 60 borrowers in 2025. That volume at the current fee structure means the protocol is generating real fee income. The 100M ARR target is not speculative in the way most DeFi protocol targets are.

What the tokenomics data shows is that even at 100M ARR with current SSF dynamics, the buyback yield caps around 3.7% of market cap. At 295M market cap and 3.3M in actual annual buybacks today, the implied buyback multiple is 89x. A 3.7% buyback yield at 100M ARR would bring that multiple to 27x. The current price requires either that compression or a governance decision to deploy more of the SSF as actual SYRUP purchases, which has not happened in either quarter since launch.

GAM Analysis is independent DeFi protocol research by @galbortam. If someone forwarded this to you, subscribe here.

Building a DeFi protocol? I do independent smart contract + economic reviews. Tell me what you are building.