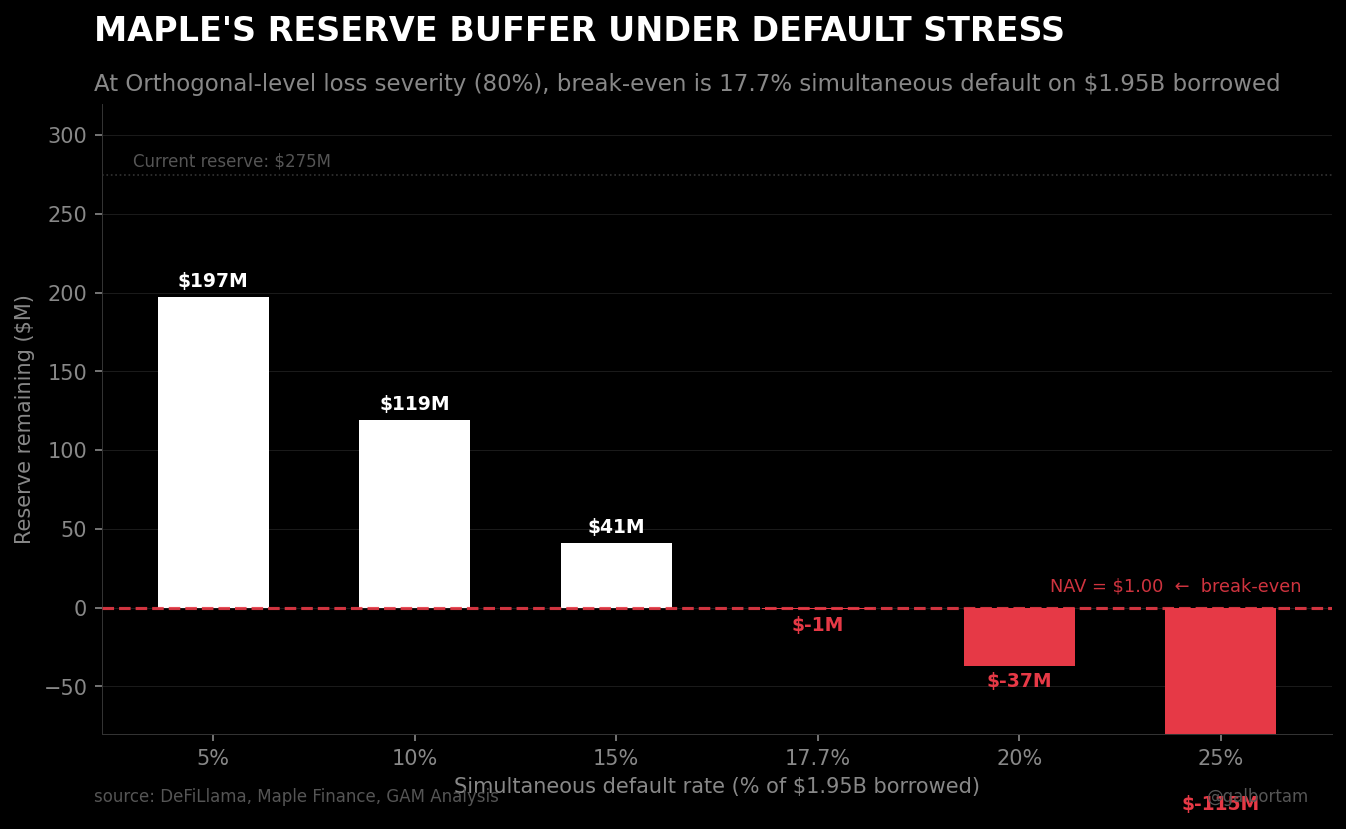

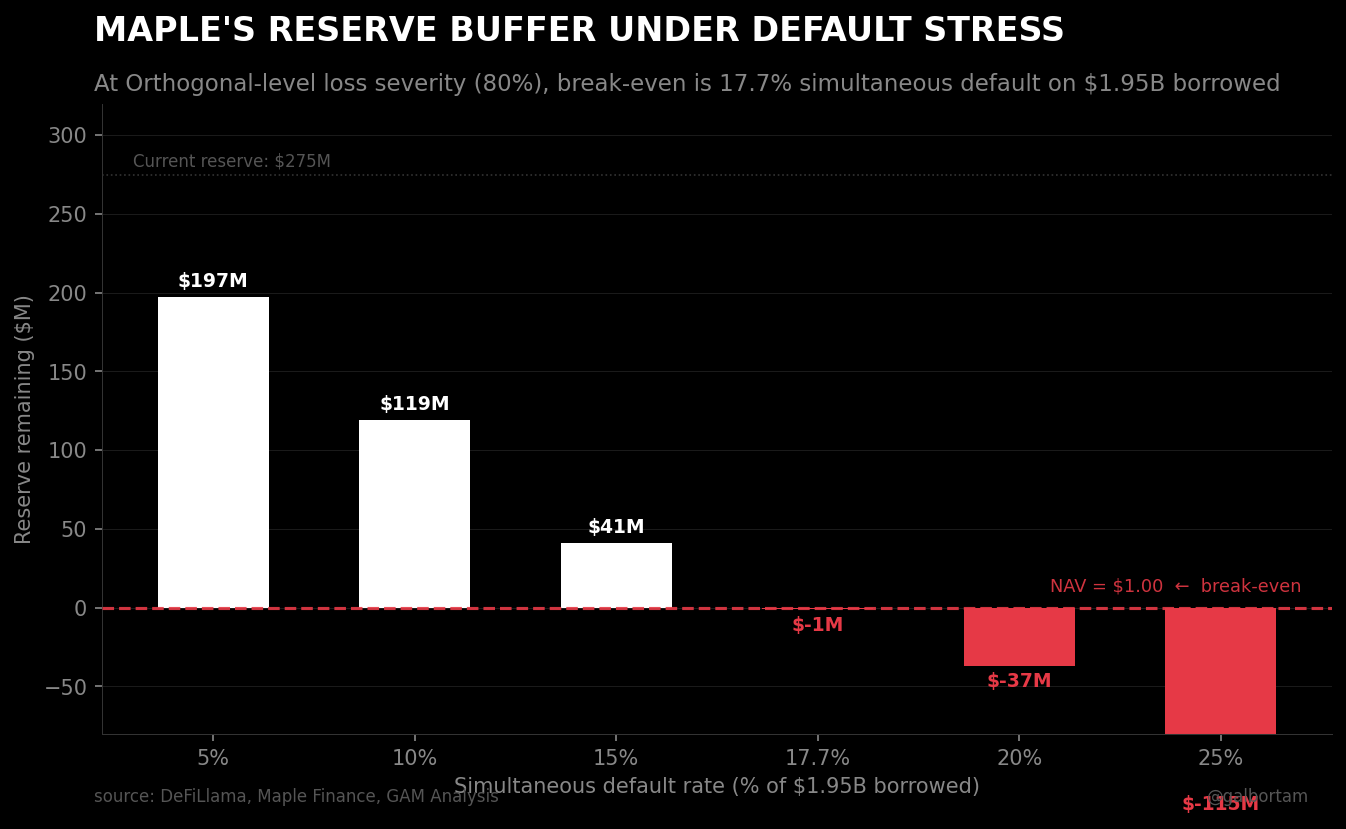

At 17.7% simultaneous borrower default, syrupUSDC NAV drops below $1.00. That calculation uses the same 80% loss severity the M11 USDC pool delivered when Orthogonal Trading defaulted in 2022.

How the model works

Maple lends depositor capital to institutional borrowers at fixed rates between 5% and 9%. Borrowers post crypto collateral. If the ratio drops below threshold, Maple liquidates.

The yield flows back to syrupUSDC depositors as an appreciating NAV. The token launched at $1.00 and sits today at $1.16, representing two years of compounded lending income.

The reserve math

Today, $1.95B is deployed in outstanding loans against $2.225B in total depositor NAV. The buffer is $275M, about 12.4% of deposits.

At 80% loss severity (the Orthogonal benchmark, and a conservative assumption for secured lending where actual recovery is typically higher), that $275M absorbs 17.7% of borrowers defaulting simultaneously. At a more realistic 50% loss severity for secured loans, the break-even rises to 28%. The exercise isn't to pick the exact number. It's to note that the margin is measured in single-digit percentage points of the borrower pool, not tens of percentage points.

Why 18% is not hypothetical

The 2022 crypto bear didn't hit one Maple borrower. It hit three inside six weeks: Orthogonal Trading, Auros Global, and Babel Finance. The undercollateralized model produced 80-cent losses in the M11 pool because there was no collateral to liquidate against.

The secured model is a genuine upgrade over 2022. The borrower profile that creates correlated stress has not changed.

Institutional crypto borrowers are concentrated in market-making and proprietary trading. During a correlated market drop, their collateral value, their P&L, and their ability to service debt all deteriorate together. You cannot model these as independent events.

A forced liquidation of $400M in crypto collateral doesn't execute at par. The assets are liquid in normal conditions and illiquid precisely when you need them most. A liquidation at that scale moves the market, recovery rates compress, and the static model starts diverging from reality.

Maple has not published its borrower concentration data. If one counterparty represents 15% of outstanding loans, the 17.7% aggregate threshold is misleading. A single default gets you most of the way there.

The integration surface

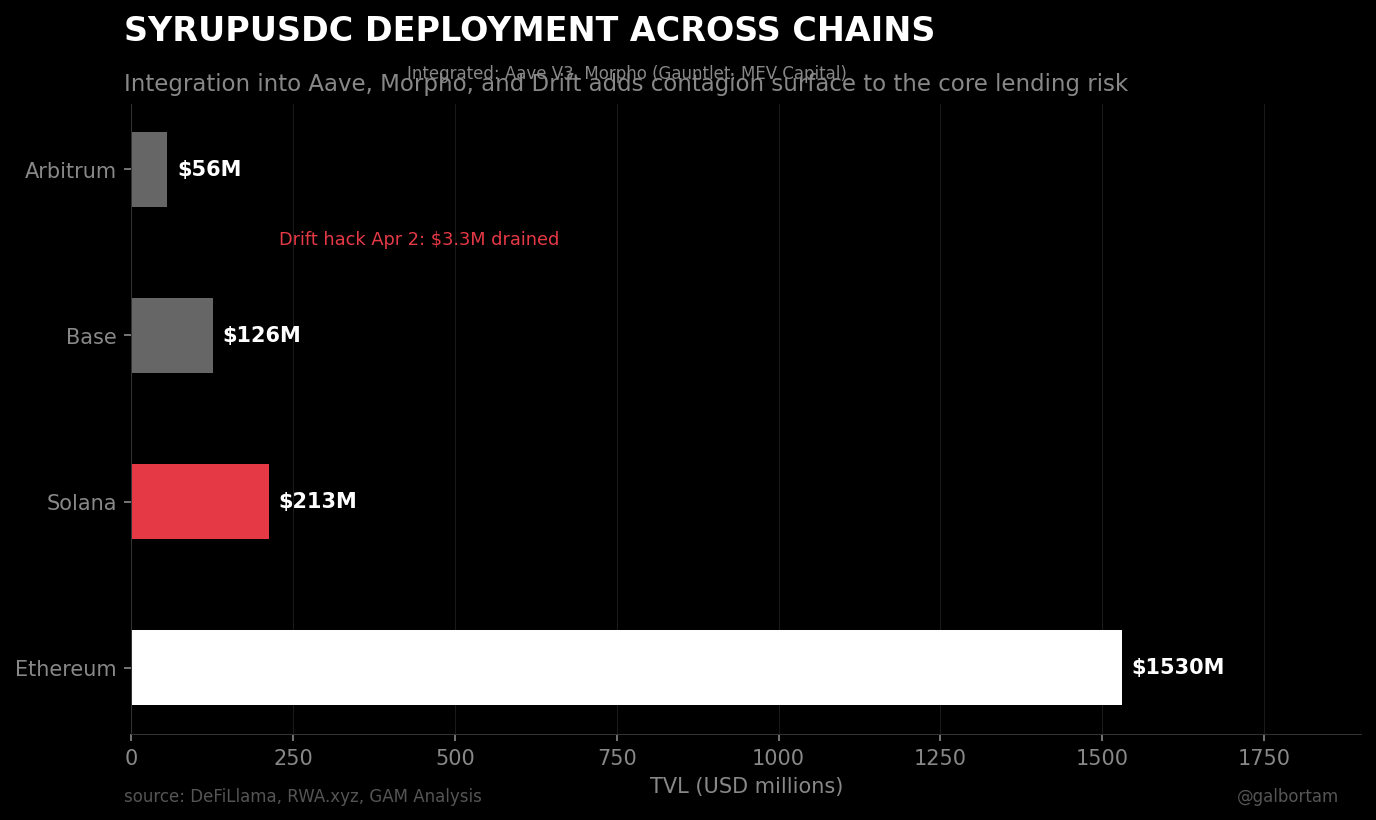

Three days ago, a hack on Drift Protocol drained 3.32M syrupUSDC from Maple depositors. Drift was using syrupUSDC as yield-bearing collateral. The technical risk of a third-party platform transferred directly to Maple's depositor base.

That 3.32M is small against $2.08B in TVL. The number isn't the point.

syrupUSDC now sits inside Aave V3 on Ethereum and Base, Morpho vaults curated by Gauntlet and MEV Capital, and Drift Protocol on Solana. The integration surface has grown every quarter since launch.

If NAV drops and downstream users are holding syrupUSDC as collateral in those protocols, they face margin calls. To cover those calls, they sell syrupUSDC. That selling pressure compounds the NAV problem through a channel that lives outside Maple's own risk model.

The feedback loop: NAV drops slightly, Aave liquidations fire on syrupUSDC collateral, more syrupUSDC selling follows, NAV drops further. You don't need a large initial shock for this to become self-reinforcing.

What the SYRUP token does and doesn't do

SYRUP staking ended in November 2025 (MIP-019, 91% community approval). The protocol replaced it with 25% of revenue directed to open-market buybacks: $615K in Q4 2025, $827K in Q1 2026.

The token is not a first-loss layer. Losses from bad debt don't come out of the SYRUP supply or governance treasury. They come out of depositor NAV. The buyback mechanism works when the protocol is healthy and provides no buffer when borrowers default at scale.

This matters for anyone holding both SYRUP and syrupUSDC: the token's performance and the deposit's safety are correlated but not aligned. A stress scenario that hurts depositor NAV also suppresses protocol revenue, reduces buyback activity, and moves token price against you. Both positions deteriorate in the same scenario.

What this means for allocators

The 2.55% base yield you see today is not the product's history. Yield compressed from 11% in 2024 to 3.72% in early 2026 to 2.55% today. Incentive-driven depositors leave when returns normalize.

Exit pressure at scale becomes a liquidity test on a fixed-rate loan book. The loans don't come due just because depositors want out.

The question to ask: what is the weighted average maturity of the current loan book, and what is the maximum redemption volume Maple can service in a 30-day window without touching the reserve?

What this means for builders

If you are integrating syrupUSDC into your protocol as a collateral type or yield source, the Drift incident is the calibration point. You inherit Maple's loan book risk and your own platform's smart contract risk. The losses land in the same place regardless of which channel they came through.

The curator model (Morpho vaults curated by Gauntlet, MEV Capital) adds one layer of monitoring but doesn't change the underlying exposure. Curators can adjust allocation. They cannot liquidate Maple's fixed-rate loans early.

What to watch

When syrupUSDC NAV drops below $1.05, watch for exit pressure from Aave and Morpho users holding it as collateral. That is when the cascade channel activates.

The primary signal is NAV, not utilization. Current 93% utilization is high but stable. The warning is a NAV move, which depends on how Maple's undisclosed borrower base performs when crypto markets fall 40-60%.

Watch for borrower concentration disclosures. Any governance proposal that reveals single-counterparty exposure above 10% changes the break-even math materially.

The second signal: redemption queue depth. If redemptions exceed the $130M in undeployed capital sitting outside the loan book, Maple faces a maturity mismatch. Depositors want out, the loans won't mature on demand. This is a structural liquidity problem with no clean resolution, and it can happen while every borrower is current.

Closing

The secured model is a genuine upgrade over what failed in 2022. The integration surface is the new risk layer, and the Drift incident three days ago is the first public signal of what contagion looks like at small scale.

GAM Analysis is independent DeFi protocol research by @galbortam. If someone forwarded this to you, subscribe here.

Building a DeFi protocol? I do independent smart contract + economic reviews. Tell me what you're building.