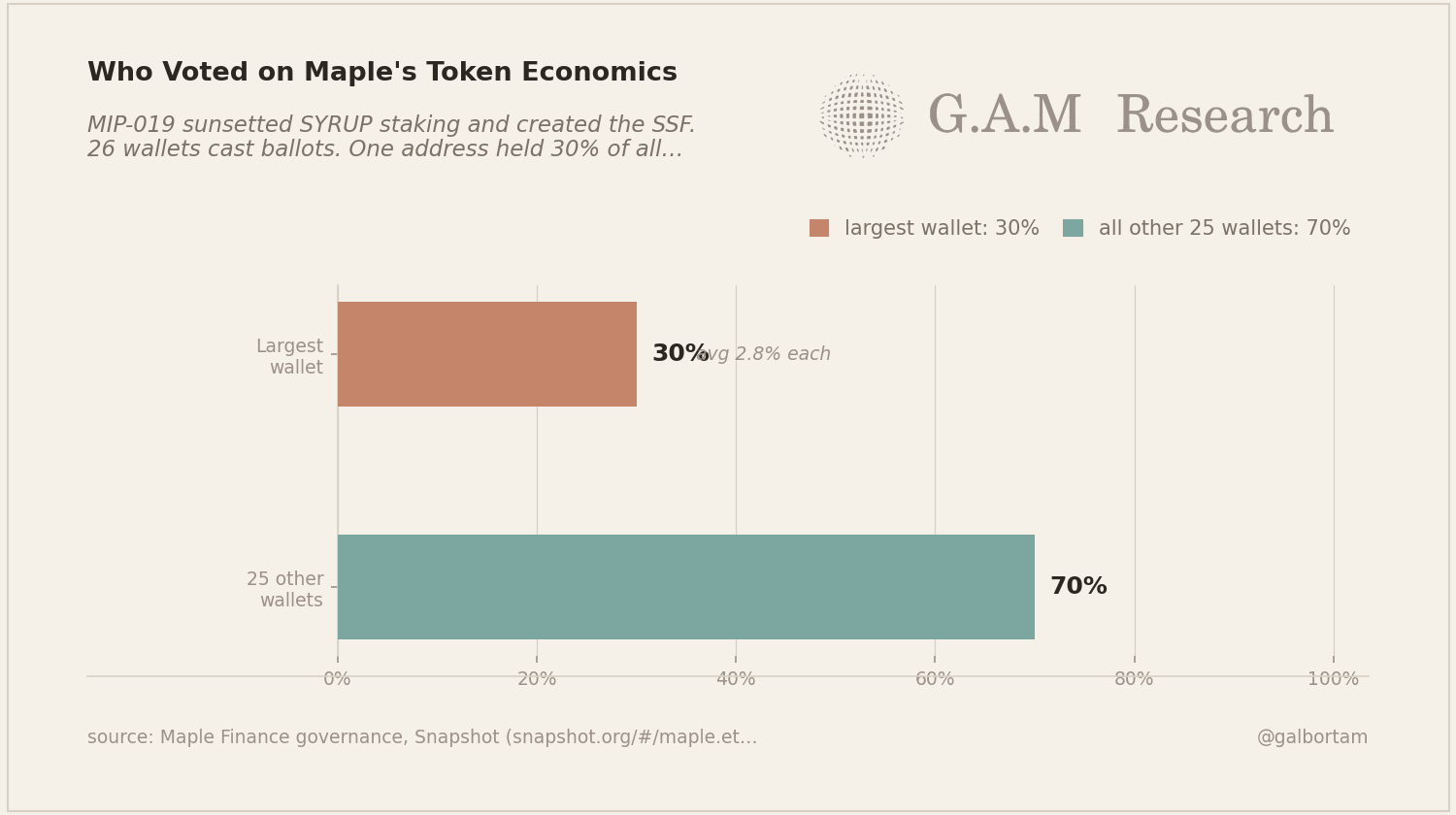

Every SYRUP buyback since November 2025 was authorized by a governance mandate approved by 26 wallets. One of those wallets cast 30% of all votes.

That vote, MIP-019, is the foundational governance decision for how Maple allocates protocol revenue to token holders. It sunset staking rewards, created the Syrup Strategic Fund, and established the SSF’s mandate with no minimum buyback ratio. It passed with 99% approval. The approval rate reflects the concentration, not the consensus.

How the governance works

Maple’s governance runs through Snapshot. Proposals require 5% of circulating supply as quorum, roughly 63 million SYRUP at current levels. Voting windows last seven days.

MIP-019 cleared quorum. Twenty-six wallets cast ballots to determine the structure of how 25% of all Maple protocol revenue would flow to token holders, indefinitely. The largest single address controlled 30% of all votes cast, leaving the remaining 25 wallets averaging 2.8% each. Thin participation and concentrated token distribution made this outcome structural, not accidental.

What MIP-019 actually decided

The mandate has two layers. First: 25% of protocol revenue flows to the SSF on an ongoing basis. Second: the SSF allocates that revenue between SYRUP buybacks, BTC treasury, and stablecoin reserves at its own discretion, with no minimum buyback ratio in the proposal text.

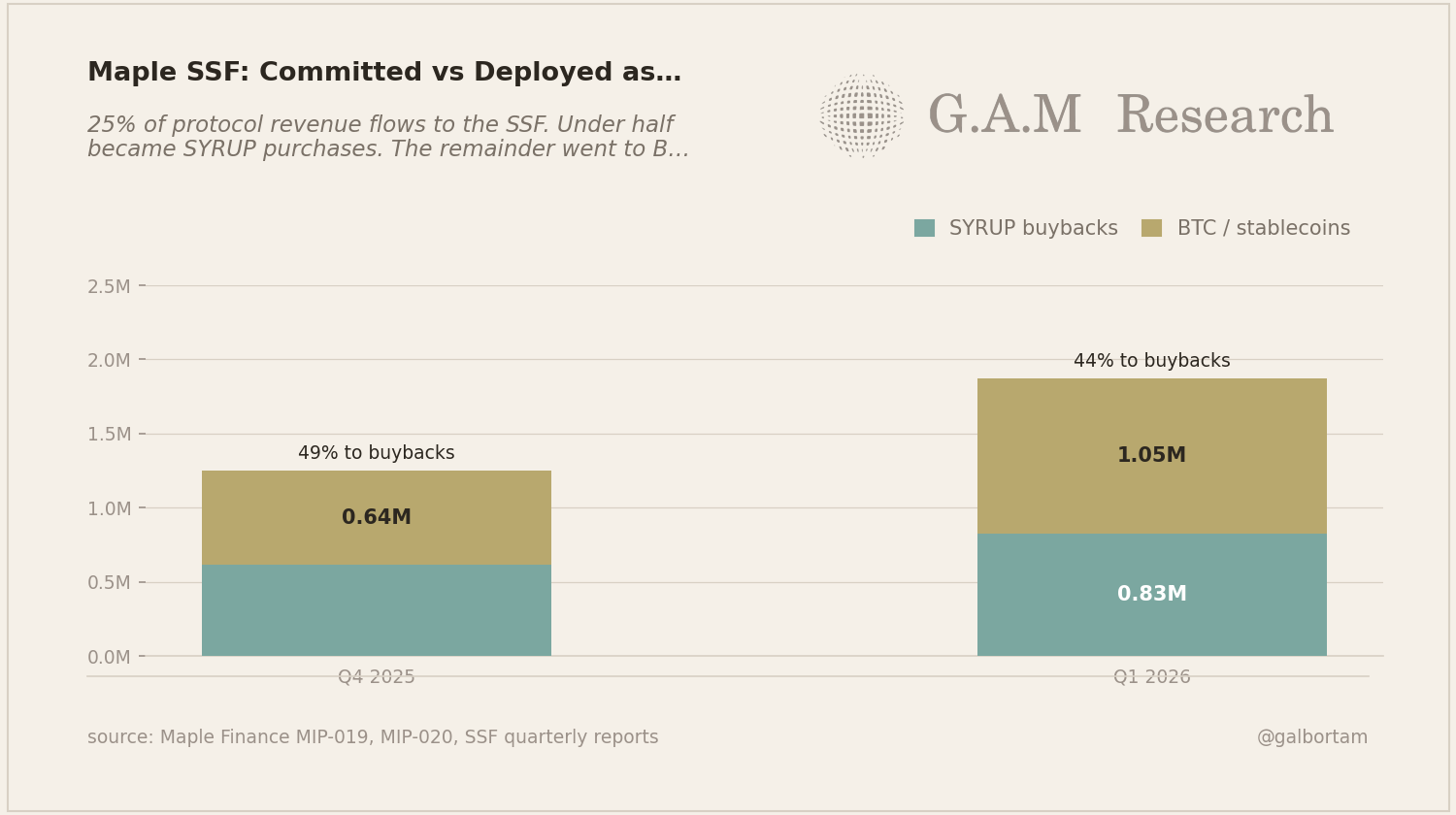

From the tokenomics analysis three weeks ago: in Q4 2025, the SSF deployed $615K as SYRUP buybacks against $1.25M committed (49%). In Q1 2026: $827K deployed against $1.875M committed (44%). The remaining 56% went to BTC and stablecoins. Treasury diversification is defensible governance. It is not a token buyback.

At current deployment rates, approximately 11% of total protocol revenue reaches SYRUP holders through actual market purchases. The 25% figure is the SSF allocation. Those are two different numbers, and the governance language that created this structure did not specify which one counts.

MIP-020 (January 2026) extended the SSF framework through H1 2026 without revising the discretion structure. The same mandate governs both quarters.

Of every $100 in protocol revenue Maple earns, roughly $11 reaches SYRUP holders through actual market purchases. The other $89 goes to depositor yield, delegate fees, Maple Labs operations, and SSF treasury diversification. That is the actual distribution, as of Q1 2026.

The pool delegate structure

Pool delegates are the credit governance layer beneath everything else. They source borrowers, conduct due diligence, set loan terms, and manage the pools depositors fund. Governance whitelists them. Governance does not underwrite individual loans.

To serve as a delegate, a minimum $100,000 SYRUP stake is required. Delegates earn 33% of establishment fees at loan origination, plus 10% of ongoing interest during the loan term. These two income streams have different temporal structures.

Establishment fees are collected at booking, not at repayment. Ongoing interest is contingent on the loan staying current. When a loan defaults, the establishment fee is already in the delegate’s account. The ongoing income stops. Depositor NAV compresses.

When Orthogonal Trading, Maple’s first pool delegate, defaulted $36 million in loans in late 2022, the establishment fees on those loans were already settled. Ongoing income stopped. Depositors absorbed the bad debt.

Orthogonal is history, and Maple’s current loan book is performing. The structure is unchanged. Delegates are governance-approved, reputationally accountable, and economically incentivized to book loans and to keep them current. The question for depositors at $4 billion AUM is whether governance-approved whitelisting and reputational accountability are sufficient risk controls at this scale, and whether the upfront fee creates any tilt toward booking over monitoring at the margin.

What this means for you

If you hold SYRUP, the effective buyback yield at current conditions is approximately 1.1% of market cap annualized: $3.3 million in buybacks against a $293 million market cap. The counter-thesis is real and worth holding. At $100 million ARR, current SSF deployment rates produce $11 to $13 million in annual buybacks. That is a 4%+ implied yield at today’s market cap. The bull case exists.

What it depends on is governance maintaining the SSF commitment through the revenue growth cycle. The SSF’s incentive to diversify into BTC and stablecoins grows with AUM, not decreases. A 26-voter DAO with no minimum buyback floor in the mandate gives you thin assurance that the commitment holds when diversification becomes more attractive.

If you supply to syrupUSDC, the pool delegate structure is the credit accountability layer you are relying on. Delegates earn upfront fees at booking and ongoing income while loans are current. Both stop at default. NAV compression from defaults falls on depositors. That structure creates alignment with loan performance, with one directional tilt worth understanding: the establishment fee is settled at origination regardless of outcome. Knowing the current loan composition, borrower concentration, and delegate track records is risk work the governance process does not do on your behalf, and most of that data is not on any public dashboard.

Second-order dynamic

If token distribution broadens as Maple grows, governance may follow. Maple launched SYRUP on Revolut on April 30, 2026, reaching 70 million users in the UK and EU. If retail access converts to distributed token ownership and eventually Snapshot participation, the 26-wallet concentration may self-correct.

Whether token ownership on consumer platforms translates to governance participation is a different question. Most Revolut users will not connect wallets to Snapshot. The path from broader distribution to functional DAO governance has no historical guarantee.

What to watch

Watch wallet participation in the next SSF governance vote. If it remains under 50 wallets, concentration has not improved with the protocol’s growth. The discretion gap in the SSF mandate is structural, not transitional.

The Q2 2026 SSF deployment data, when published, is the number that matters most for SYRUP holders. When the buyback share of SSF falls below 40%, effective yield at current ARR drops below 1%. Below 30%, the buyback program is a narrative. Both thresholds are observable on-chain.

When MIP-020’s follow-on governance vote closes, check the wallet count. If it is still under 50, the governance concentration that approved the original mandate is the mechanism, not an artifact of early-stage bootstrapping.

GAM Analysis is independent DeFi protocol research by @galbortam. If someone forwarded this to you, subscribe here.

Building a DeFi protocol? I do independent smart contract + economic reviews. Tell me what you’re building.